Access to global markets is increasingly conditional on meeting social and environmental standards in a number of strategic economic sectors relevant to Southeast Asia. Although linking trade to environmental and labour standards is not new, what has changed is the extent to which diverse, often competing public and private socio-environmental standards are reshaping, albeit unevenly, global supply chains in key commodities produced in these countries while cross-cutting demands to improve socio-environmental practices in these sectors enter supply chains from many sources and levels, often taking by surprise targeted economic actors and their governments. Such pressures have been in the making for over two decades but were uneven, diffuse, and mostly emanated from non-profit actors, and so governments missed, misinterpreted or dismissed these until about some years ago when their combined, interactive effects became visible and significant. In such complex situations, economic security requires industry resilience, which at the least, requires fundamental recognition that socio-environmental standards are here to stay, will likely escalate and will, therefore, require changes to local production processes even as states use various diplomatic tools to address more immediate barriers to market access.

In July 2020, in the midst of the Covid-19 pandemic when disposable surgical gloves were a vital commodity worldwide, the United States Customs and Border Protection (CBP) withheld a shipment of gloves produced by Malaysian company Top Glove, one of the world’s largest manufacturers of rubber gloves, on the grounds that their production involved forced labour.[1] A second case in 2020 involved palm oil shipments to the United States. Similar ‘withhold release orders’ (WROs) were placed on palm oil produced by Malaysia’s largest multinational plantation corporations, Felda Global Ventures and Sime Darby, respectively in September and December 2020, on grounds that their production operations involved forced labour.[2] Downstream manufacturers then reportedly blocked palm oil from both corporations from entering their production operations in the US and elsewhere in Europe, Australia and Japan on concerns that their own products would be shunned if they incorporated such tainted palm oil.[3]

If economic security is “aimed at ensuring minimal damage to a set of economic values”,[4] then economic security for most Southeast Asian states will encompass reliability of access to global markets for key exports produced from economic sectors whose continued functioning is deemed to be of strategic importance for economic growth and development. Despite markets remaining broadly open, the past few years have shown that access to global markets is becoming increasingly conditional on meeting ethical standards of production. Social and environmental standards have the potential to reorder global supply chains that extend into consumer markets in the developed world. Such trends will be of special concern in Southeast Asia. Although China is now the second largest market for the Association of Southeast Asian Nations (ASEAN) absorbing 14.2% of its exports in 2019, the US and the European Union (EU) remain the next two important markets absorbing respectively 12.9% and 10.8% of ASEAN exports in 2019. More than market share, however, are their status as global norm setters. Minor disruptions to market access may not matter in terms of material earnings but could well have a disproportionate impact on the evolving normative structures of the global economy within which state and economic actors must operate. If global market access remains a key economic security goal for Southeast Asian states reliant as they are on exports from sustained production in strategic economic sectors, then serious attention must be paid to enhancing environmental and social standards, both for their intrinsic worth and because not doing so will pose market and reputational risks to precisely these sectors.

What is new about these ethical standards?

To be sure, linking trade to environmental and labour standards is not new. What has changed as we move into the third decade of the twenty-first century is the extent to which global supply chains are becoming more complex as a result of ethical standards of production. A diverse, often competing, array of public and private socio-environmental norms, rules and standards are reshaping, albeit unevenly, global supply chains in key commodities produced in the developing world. This phenomenon is intertwined with the multi-layered, cross-cutting demands to improve socio- environmental practices in production and consumption that come from many sources and levels such as state authorities, supply chain actors, transnational non-profit and civic organizations, consumer sentiment and lately financial market processes. The multi-way interaction of these different demands and pressures can leave targeted economic actors and their governments caught off- guard. Such pressures are not a recent development but have been in the making for over two decades but were uneven, diffuse and mostly emanated from non- profit actors. As such, they were easier to miss, misinterpret or dismiss until about some years ago when their combined, interactive effects became visible and significant.

Such emergent dynamics suggest that traditional ideas of discrete states interacting linearly with other states over market access need correction to incorporate the notion of states as one among many actors interacting within social spaces such as supply chains that transcend state boundaries. In such spaces, varying permutations of authority may be exercised in several inter- linked ways: hierarchically through state diplomatic, legislative or regulatory actions; through the market power of economic actors operating in and through global production networks, supply chains and latterly financial markets; and especially through the information, knowledge and discursive capabilities that empower transnational actors in their advocacy, surveillance and soft law activities. These trends create a complex, often unfamiliar terrain for states and producers operating in a region like Southeast Asia where economic growth remains rooted in the exploitation of labour, land and nature and where states had been able in the past to block or deflect external and domestic demands for change, particularly when they came from non-governmental organizations (NGOs).

Today, we see at least three key sources of external demands and pressures to conform to ethical standards in economic production: (a) bilateral and plurilateral free trade and economic partnership agreements negotiated with developed countries that require conformity to mutually agreed environmental, labour and human rights standards; (b) socio-environmental policy or legislation enacted in developed states that restrict imported products not meeting these internally developed rules and laws; and (c) transnational governance challenges led by transnational, non-state actors whose advocacy, surveillance and soft law activities are helping to embed ethical standards as the wider rules of the game in and across various supply chains.

Both the US and EU have adopted what may be deemed WTO-plus or next generation comprehensive trade agreements that incorporate various mixes of social and environmental rules and standards. Although such agreements may be onerous, these commitments have at least been formally negotiated and adopted by both parties. It is when external demands and pressures emerge from outside such mutual agreements that affected corporations and governments of producer countries seem to be taken unawares. Consequently, it is the latter two sources identified above – national regulatory actions and transnational governance practices – that pose the more pressing challenge for states in this region. Governments have not been sufficiently attentive to both the socio- environmental damage caused by economic production in their countries and to the ways in which newly constituted “ethical markets” can shrink the kinds of production practices permissible as well as state policy spaces.

A complex terrain

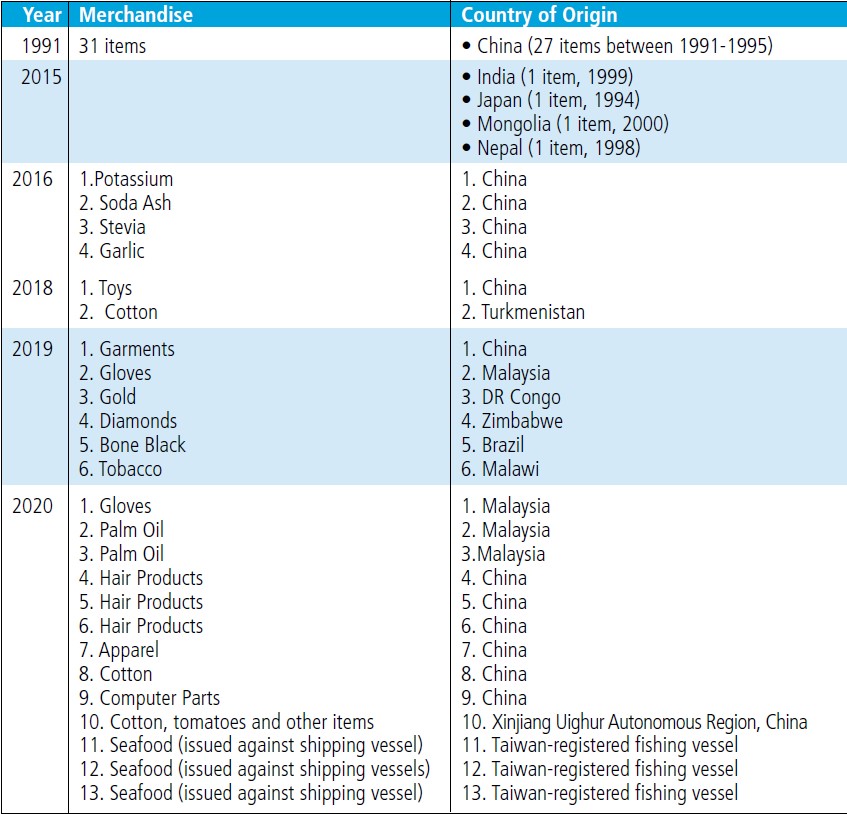

The WROs issued by the US CBP reflect these complex dynamics. WROs are used by the CBP to enforce Section 307 of the US Tariff Act of 1930 that prohibits the import of goods mined, produced or manufactured using forced, including prison labour and child labour. However, only 31 WROs had been issued in the fifteen years from 1991 and 2016 due to an exemption clause in Section 307 that allowed imports of such goods to meet domestic demand. The repeal of the exemption clause in 2016 and the establishment of a permanent forced labour office within the CBP saw a sharp rise in CBP actions against forced labour.[5] Between 2016 and 2020, 25 WROs were issued against products, corporations and sectors employing forced labour practices (see table below).

This trend is expected to grow with the US Congress increasingly intent on enforcing action against forced labour practices worldwide. Equally important, transnational human/labour rights activists and organizations, which had previously lobbied hard for the 2016 exemption repeal, are leveraging on the CBP’s enhanced role to identify and take action against forced labour situations in various local sites in the developing world. The CBP often relies on and is allowed to use third-party investigations to inform its decisions to issue WROs. Moreover, it is allowed to accept reasonable rather than conclusive evidence of forced labour practices.[6] The lower standard of evidence has aided exposés of forced labour for which conclusive evidence is often difficult and dangerous to obtain. More formal, internal investigations undertaken by governments of the affected industry or by the named company often corroborate the evidence used by the CBP and can lead to the necessary changes in labour practices. But there are also concerns about the reliability, accuracy and transparency of the evidence upon which WROs are issued. Industry observers have questioned the evidence used by the labour rights NGO that petitioned the CBP to issue the 2020 WRO on Sime Darby, the world’s largest certified producer of sustainable palm oil with multiple international sustainability certifications.[7]

Withhold Release Orders (WROs) issued by United States Customs and Border Protection, 1991-2020. Note: some of these remain active while others have been revoked, usually following remedial action deemed satisfactory by CBP authorities. Source: Author’s compilation from CBP website.

The EU’s commitment to strengthening its internal socio-environmental legislation and regulatory agenda and to extending these outside the EU, both closely informed by substantial input from transnational actors, offers salutary lessons for the region. Under the EU’s revised Renewable Energy Directive (or RED II) that came into force in December 2018, palm oil would not be deemed a sustainable biofuel from 2030 that member states could count in their sustainable biofuel mix.[8] The first RED adopted in 2009 had been roundly criticised by environmental NGOs for ironically sparking a massive expansion in palm oil production in tropical zones, and with it, deforestation. Palm oil’s substantial price and yield competitiveness had given it a significant edge as a biofuel feedstock over rival vegetable oils. The situation changed from 2018 when palm oil was the only vegetable oil frozen out of RED II because of its allegedly high carbon footprint. However, the model used to determine palm oil’s greenhouse gas emission status incorporated a controversial measure on indirect land use change (ILUC), which includes estimates of how much more forests would be displaced by the planting of additional food crops if palm oil were diverted from food to biofuel use.[9] That the ILUC is contested even within the NGO and scientific communities reveals the uncertainty and complexities in measuring and benchmarking unsustainable practices.

The Malaysian and Indonesian governments are deeply concerned over market access and the risk to the reputation of an industry regarded as a strategic sector for their economies that also provides livelihoods for the small farmers who produce about 40% of palm oil. Seeing the EU move as primarily aimed at protecting European producers of competing vegetable oils such as rapeseed and sunflower, these governments have filed a legal action at the World Trade Organization (WTO) claiming the singling out of palm oil constitutes a discriminatory trade practice. In addition to Indonesia, Colombia, the fourth largest producer of palm oil, has joined Malaysia in its formal consultancy meetings with the EU, part of the WTO’s dispute settlement process, to clarify the EU position on palm oil.[10] Indonesia and Malaysia also blocked the formation of a formal strategic partnership between ASEAN and the EU until late 2020, only removing their objections after the EU agreed to further examine the sustainability of all vegetable oils. These governments are also seeking alternative, less ethically demanding markets for palm oil in China, South Asia and the Middle East that will accept their respective national certification standards to ensure reliable market access going forward, especially in the light of further initiatives against imported deforestation into European and other developed country markets.

The EU’s 2020 “Farm to Fork Strategy” (F2F) is especially concerning. The extension of ethical production standards to govern trade in food items will have serious repercussions for Southeast Asian producers and exporters of agri-food products.[11] The F2F strategy, which drew on NGO research and advocacy, is based on the contention that agricultural expansion drives 80% of global deforestation, with palm oil, soy and beef being critical sources of such deforestation. EU actions on environmental and social standards are, therefore, expected to set global benchmarks for a range of food sectors and for consumption choices. Due diligence legislation, expected in other parts of Western Europe and the UK to keep out imported deforestation, adds another layer of environmental, specifically deforestation standards, into regulatory and legislative agendas in the developed world with substantial implications for companies and countries producing and exporting agricultural commodities and manufactured items. At the same time, such actions contribute to ethical standards becoming embedded within various supply chains.

Fisheries, an important economic sector in Southeast Asia, has also been singled out in the EU’s F2F strategy in order to reduce illegal, unreported and unregulated fishing and enhancing the sustainable management of global fish and seafood resources. The experience of the Thai shrimp industry reveals the unanticipated impact such actions might generate. Thailand lost its competitive position as the world’s second largest shrimp producer partly due to health/ safety concerns and partly due to revelations of the adverse environmental and social consequences linked to the shrimp supply chain.[12] Exposure of human rights and labour abuses on the fishing boats that supply feed to the Thai shrimp industry in 2014, even if not directly a practice of shrimp cultivators, was sufficient to impact shrimp exports following a formal warning from the EU over these practices. Even without a formal ban, the extensive media coverage of this case coupled with the regulatory attention paid to the industry saw sharp declines in Thai shrimp exports to the EU. Even when the EU warning was removed, the industry never fully recovered and continues to face NGO criticisms over the extent of its socio-environmental harms.

These cases show how diffuse events can have disproportionate effects, especially with 24-hour global media and social media. This is not to dismiss the seriousness of the socio-environmental problems discussed here, but simply to point out how enhanced media, regulatory and even scientific attention can complicate the search for sustainable solutions to these problems. In the palm oil case, the intense scientific and regulatory scrutiny into palm oil may have inadvertently diverted attention away from other commodities such as soy and beef that are said to have as bad or worse carbon footprints.[13] Despite boasting one of the more comprehensive voluntary sustainability standards (VSS) addressing deforestation, carbon emissions, and social issues such as land and labour rights, the palm oil VSS – the Roundtable on Sustainable Palm Oil (RSPO) – ironically ends up as a marker of corporate greenwashing as every act of corporate transgression is held up as evidence of a recalcitrant industry that can never be reformed.[14] It does not help that such globally accepted standards have yet to extend beyond more than a quarter of the palm oil industry while Indonesia and Malaysia have been too quick to dismiss sustainability problems in their respective industries, further worsening producer credibility. Pronouncements by prominent retailers and global brands that they are “palm oil free” reinforce these sentiments as does the “palm oil free movement”. The Palm Oil Free Certification Trademark launched in 2017 now covers 1,450 products and is recognized in 20 countries.[15]

Implications for economic security

While there may be elements of convenient green protectionism behind some of these socio-environmental agendas and trade conflicts, it is unwise to simply dismiss these as protectionism buttressed by activist NGOs while ignoring the point that global supply chains of importance to the Southeast Asian political economy – agricultural commodities, food products, fisheries, manufacturing items such as gloves, garments and footwear, among others – are already facing demands and pressures to conform to ethical production standards. Supply chains themselves are, moreover, becoming highly interconnected, complex systems.

Governments are not standing still. Their responses combine both tactical and strategic actions, working to reverse individual market access problems as they appear while addressing the wider social and environmental problems that undermine global market access for their key sectors. Tactical moves to redirect exports to less demanding final markets cannot be permanent solutions, moreover. Complex systems are, after all, noted for being hard to predict because of the multiple layers of interaction among their actors and component parts.[16] They require more strategic action that recognizes that the Southeast Asian political economy is deeply connected to both more and less ethically demanding markets that are themselves dynamically interconnected. In a situation of such complexity, strategic action requires a focus on industry resilience. At the least, resilience requires fundamental recognition that socio-environmental standards are here to stay, will likely escalate and will, therefore, require changes to local production processes even as external diplomatic tools are tactically and strategically employed to buy time for fundamental domestic changes to take root.

References

[1] Free Malaysia Today (2020) “US adds Malaysian rubber gloves onto list of goods produced with forced labour”, 14 October, available online

[2] US Customs and Border Protection “Withhold Release Orders and Findings”, available online

[3] Chu, M.M. (2021) “Buyers shun major Malaysian palm oil producers after forced labour allegations”, Reuters, 8 February, available online. See also, The Malaysian Reserve (2021) “WROs on Malaysian palm oil have ripple effect, says expert”, 15 February, available online

[4] Nesadurai, H.E.S. (2006) “Conceptualising Economic Security in an Era of Globalisation: What does the East Asian Experience Reveal?”, in Nesadurai, H.E.S., (ed.), Globalisation and Economic Security in East Asia: Governance and Institutions, London and New York, Routledge, 3-22.

[5] Roggensack, M., Syam, A. (2020) Withhold Release Orders, in Three Acts: Heralding A New Enforcement Era, available online

[6] U.S. Customs and Border Protection (2016) “Forced Labor Enforcement, Withhold Release Orders, Findings, and Detention Procedures”, Commercial Enforcement Division Forced Labor Enforcement Fact Sheet, available online

[7] Busfield, A. (2021) “US palm oil ban baffles industry watchdogs”, Asia Times, 8 March, available online

[8] EU Science Hub (2018) “Renewable Energy – Recast to 2030 (RED II)”, available online

[9] See Mayr, S., Hollaus, B. and Madner, V. (2020) “Palm oil, the RED II and WTO law: EU sustainable biofuel policy tangled up in green?”, Review of European, International and Comparative Environmental Law 2020(00):1–16.

[10] “Govt committed to legal action against EU over palm oil.” (2021), The Edge, 19 March, available online

[11] European Commission (2020) Farm to Fork Strategy: For a Fair, Healthy and Environmentally-Friendly Food System, available online

[12] Boston Consulting Group (2019) A Strategic Approach to Sustainable Shrimp Production in Thailand: The Case for Improved Economics and Sustainability, available online

[13] Meijaard, E. et al. (2020) “The Environmental Impacts of Palm Oil in Context”, Nature Plants, 6: 1418-1426.

[14] Nesadurai, H.E.S. (2018) “New Constellations of Social Power: States and Transnational Private Governance of Palm Oil Sustainability in Southeast Asia.”, Journal of Contemporary Asia, 48(2): 204-229.

[15] SIIA (2020), ESG in Practice: A Closer Look at Sustainability in ASEAN’s Palm Oil and Pulpwood Sectors, Singapore, Singapore Institute of International Affairs.

[16] Goh, E. and Prantl, J. (2017) “Dealing with Complexity: Why Strategic Diplomacy Matters for Southeast Asia”, East Asia Forum, 9(2): 36-39.

The ongoing development of Sino-Gulf relations, driven by China’s deepening ties with the states of the Gulf Cooperation Council (GCC), represents a significant shift... Read More

Come ogni fenomeno economico e sociale nella Repubblica popolare cinese (Rpc), anche i mezzi di comunicazione di massa del Paese hanno registrato negli ultimi... Read More

Lo sviluppo dell’intelligenza artificiale (Artificial Intelligence, AI) è al centro dei dibattiti politici, economici e dell’innovazione di moltissimi paesi. La Cina è senza dubbio... Read More

Short or rhythmic slogans to convey ideals have been employed by the Chinese Communist Party since its foundation to support the national narrative. In... Read More

This article presents some research evidence taken from the Future Stakeholders Project survey conducted during the academic years 2021/22 and 2022/23 by the Italy-China... Read More